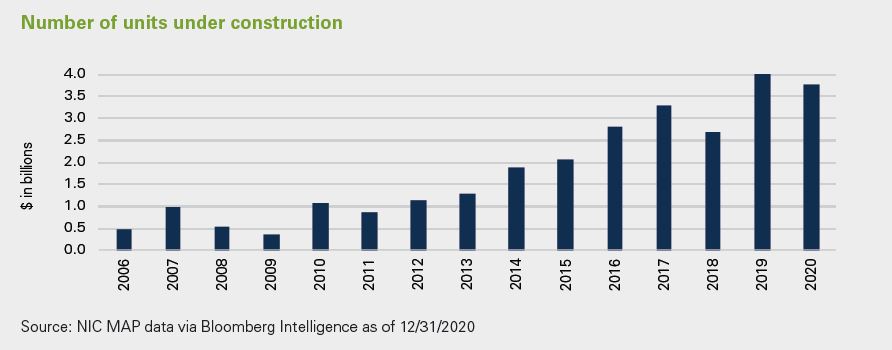

Challenges and trends in senior living and care

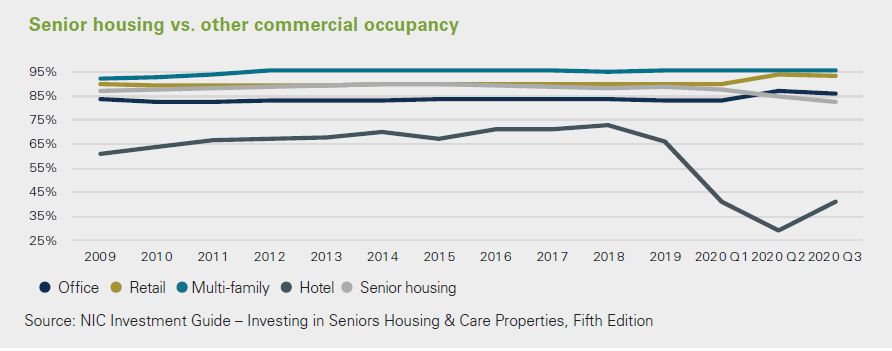

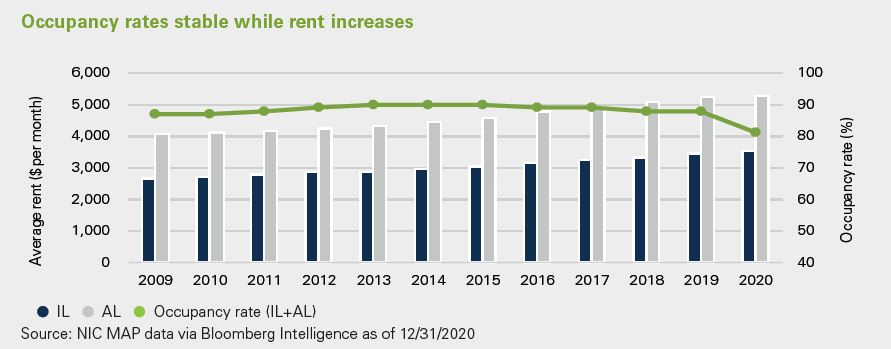

Soft occupancy rates

While 2020 was a trying year, many of our operators inoculated residents and staff per the CDC’s recommendation that they be among the first recipients of the vaccine. As you can imagine, a vaccine more than lifted the spirits in many of our communities. Given the salacious headlines and doomsday projections in March 2020, one might have expected senior living to be wiped off the map, but it wasn’t, thanks to the industry’s resilience and federal stimulus dollars.

On a positive note, the pandemic has strengthened the industry’s infectious disease policies and procedures which has brought lasting change for the better. For example, the industry has been remarkably slow to adopt telehealth; however, telehealth visits have gone from approximately 3% pre-Covid-19 to more than 50% currently since the pandemic began. The dramatic positive shift was made possible by Congress passing bills in the spring of 2020 which now allow telehealth to be covered by Medicare.

The reality is senior that living is a high turnover model that’s resilient and your average high acuity setting hasn’t seen many more deaths than a typical year. Statistically, through December 2020, nationwide occupancy for independent living and assisted living decreased to 83.5% and 77.7%, respectively. Occupancy has decreased for independent and assisted living, 6.2% and 7.5% since the pandemic began. It’s worth noting, the rate of decline from month to month is decelerating for both independent and assisted living and primary markets have seen a higher rate of decline than the secondary markets we typically invest in.8

Quality care

Preparing for the silver tsunami comes with a host of challenges, and one of the greatest is hiring and retention of a well-trained workforce to provide quality care. In today’s low unemployment environment, the cost of quality labor continues to rise along with new state minimum wage standards. And while many providers have a passion to serve seniors, a quality wage for the provision of quality care is critical.

With expectations that 1 million to 2.5 million additional caregivers will be needed between now and the end of the next decade to counter this lack of supply, many providers are offering key employee retention plans with attractive benefits packages including health insurance, paid time off, transportation, 401(k) plans and more.9

Affordability and the path to Medicare

As baby boomers age, there will be an increasing need for low cost senior housing and more subsidies needed for health care costs for those who have not adequately saved for retirement. While many developer projects focus on private pay or market rate projects, some are developing projects to serve the affordable segment of the aging population.

Medicare continues to be a major provider of health care for seniors. In 2018, there were 61 million people receiving health care coverage through Medicare, with spending reaching $590 billion, approximately 14% of total national health care spending.10 While Medicare typically covers nursing home stays, there is no requirement that Medicare must pay for assisted living. As a result, the level and type of support varies widely for Medicare- assisted care from state to state.

Medicare Advantage, which offers private, Medicare-approved insurance, has experienced headwinds resulting in seniors receiving lower daily reimbursement rates, shorter lengths of stay for care and more referrals to home care instead of inpatient rehabilitation facilities.11

Uneven regulation

While the skilled nursing industry is highly regulated at the federal and state levels, regulation of assisted living and memory care facilities differs by state and is not uniform. Examples include building design standards, licensures and staffing requirements. This makes underwriting for investors a challenge which is only mitigated by experience and knowledge of regulatory idiosyncrasies.

CONs – another layer of regulation

In addition to a state licensure, a certificate of need, or CON, is an endorsement that numerous states require before approving the construction of a new health care facility. From an underwriting perspective, CONs can create investment opportunities because they can create barriers to entry.

July 30, 1965: With former President Truman at his side, President Lyndon Johnson signs the Medicare bill into law.

July 30, 1965: With former President Truman at his side, President Lyndon Johnson signs the Medicare bill into law.

Senior Living - Investing in a growing population