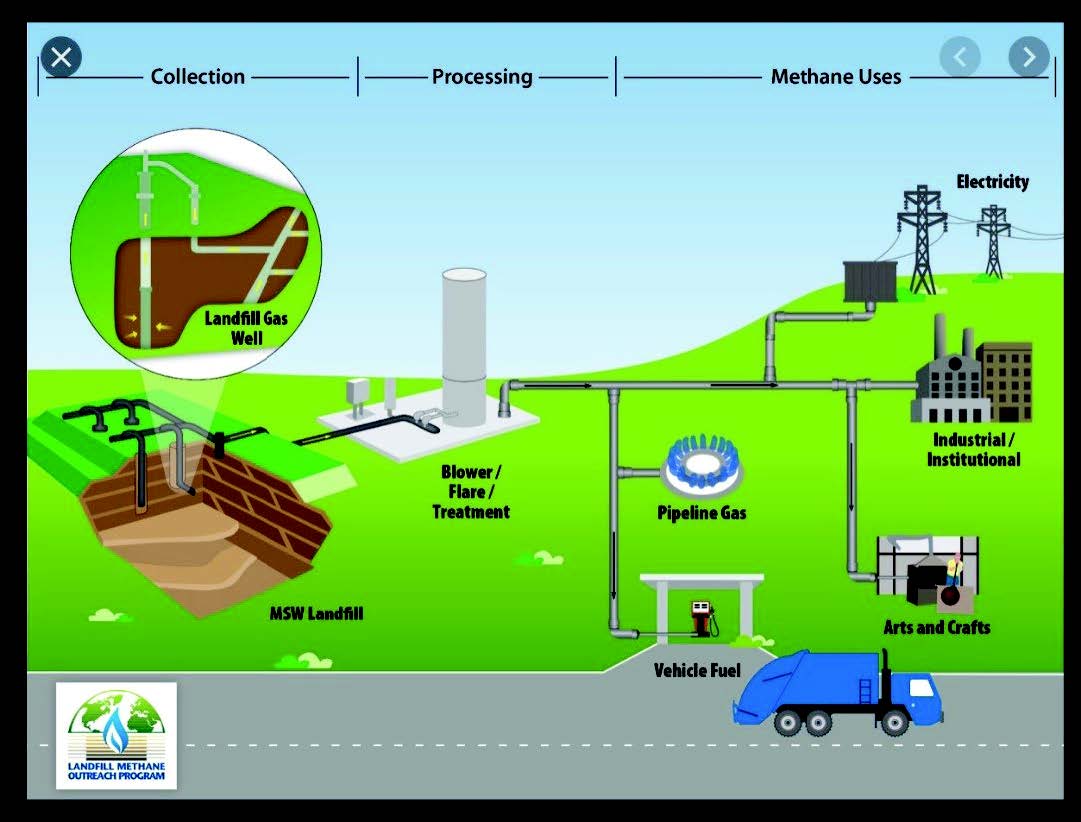

What technologies exist to capture and use these methane emissions?

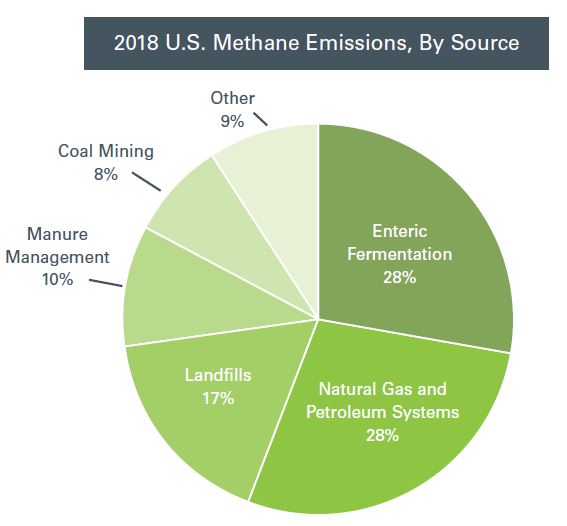

The ability to capture methane at landfills and convert it into either electricity or to clean it up sufficiently to sell it to the natural gas stream has existed for several decades. Yet even after decades of work, the EPA states that only 565 U.S. landfills of a total of 2,627 currently capture methane. In other words, barely 20% of landfills capture methane emissions, and the rest let it pollute the atmosphere exacerbating our climate change issues.

In a similar fashion, we can capture methane from animal farms by utilizing anaerobic digestion of the manure and other waste from processing that would otherwise be dumped into landfills. Collecting organic waste and recycling it has barely started in most places in the country. Some metropolitan areas have recently banned organic waste from going to landfills. We applaud this move. However, the construction and operation of facilities to compost this material and capture the methane emissions is just now gaining true momentum. We believe this will become another rapidly growing sector of the market. These facilities can turn cost centers (paying to haul off waste) into profit centers as the renewable natural gas is captured and sold into the natural gas stream or used to generate electricity. Further, in many areas, renewable credits can augment the economic returns for investors.

The technology for anaerobic digestion has been utilized worldwide for many decades. Until recently, the implementation has been slow in the U.S., but significant growth is now occurring. For example, according to AgStar, 17 new facilities came online in 2020 with 60 more under construction currently. That’s over 25% growth in the last year. AgStar estimates that there are about 8,100 large farms and dairies in the U.S. that have sufficient scale to achieve a profitable anaerobic digestion facility, versus only about 300 such facilities currently in existence, so there is much room for continued growth.

We can also capture methane from sewage treatment facilities. Instead of letting these sources generate toxic greenhouse gases, we can turn this waste into three valuable byproducts: 1) methane that can be used for electrical production or injected into the natural gas stream, 2) purified water and 3) solid waste that can be a tremendous organic fertilizer. In the EPA’s most recent research, conducted by the Water Environment Foundation in 2015, there were 1,268 anaerobic digester facilities operating at U.S. wastewater treatment facilities, representing only about 8% of the approximately 16,000 municipal wastewater treatment plants in the U.S.

Finally, after reviewing how few methane-capture facilities are operational in the U.S. at landfills (565), on farms (300), and at waste water treatment plants (1,268), it is worth noting that AgStar referenced a staggering statistic in a 2020 report that Germany alone has an estimated 8,000 commercial anaerobic digesters in operation. In other words, the U.S. is far behind other industrialized nations in this regard, and catching-up may take many years of sustained growth.

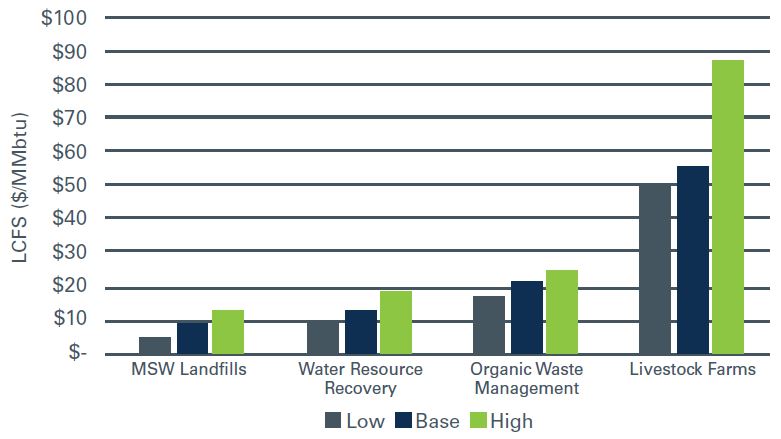

Sources: CARB, EIA, Credit Suisse estimates

Sources: CARB, EIA, Credit Suisse estimates

Waste Transition: Saving the Planet and Providing Economic Prosperity